Alphabet (Google) Deep Dive

What makes this stock such an interesting option for investors who think long-term

So let’s just address the elephant in the room right here:

I don’t own any Google stock. I don’t intend to set up a position anytime soon (mostly because I am already heavily invested in tech and have 3 out of the 7 of the Magnificent 7).

They have been written about ad infinitum by people far smarter than I. You can find plenty of other analysts here on Substack who have better credentials than I and a much better understanding of the stock market and how it works.

It isn’t exactly an exotic growth stock that has the potential to turn into a 100-bagger. Alphabet is hardly what we might call an explosive growth stock anymore… Heck, it offers a small dividend, which is not something that screams explosive growth!

(If you’re a numbers guy, just scroll to the end where I go through a few of what I believe to be the most pertinent figures.)

My Current Portfolio

Having spent a considerable amount of time in the field of online stuff and finance in particular, I've come to understand that all claims are mere rhetoric until they are supported by tangible evidence. To that end, I am creating this post to hopefully allay your fears regarding whether I practice what I will eventually preach! This initial post (which…

So, you might read that and think, What on earth could I possibly offer to you, dear reader? Well, it’s a valid question, so here goes:

I am unbiased and try to remain positive on a stock regardless of what others might believe. I also happen to perform my own research based on my own way of investing, which is to look long-term, understand the fundamentals, and explore a company beyond merely the numbers.

If that sounds like something you want to read, then have at it. Be forewarned, this is a rather in-depth analysis, and if you enjoy it, I only ask that you subscribe so that you can receive further updates on other exciting stocks based on similar analyses.

Why Google?

Before getting into things too deeply, it’s worth noting briefly why I have chosen Google as this week’s stock deep dive. You can read briefly in my first weekly newsletter that I chose Google as my pick of the week for several reasons. (From now on, I will use the name Google as a catch-all for the actual company, Alphabet.).

It has room to grow.

It’s widely accepted to be undervalued right now based on various metrics.

They have an abundance of resources at their disposal to expand beyond their primary focus on search and advertising.

So, with that out of the way, let’s take a deeper look at why Google might just turn out to be an investment that has legs.

Here are some figures to pique your interest (I primarily conduct my research using StockUnlock).

Company Overview

Alphabet Inc., established in 2015 as the parent company of Google, is a global technology conglomerate headquartered in Mountain View, California. Founded in 1998 by Larry Page and Sergey Brin, Google transformed the internet with its search engine and has since expanded into a wide array of products and services. Alphabet’s structure allows Google to focus on its core businesses while other ventures operate independently under the Alphabet umbrella.

Key Products and Services

This is where things start to become a little more intriguing than your average tech company. In many ways, Google is far more diversified than most people understand.

Google Search commands almost 90% of the global search engine market, serving as the primary gateway for online information (StatCounter).

YouTube: The world’s largest video-sharing platform, with over 2.5 billion monthly active users, generating significant advertising and subscription revenue.

Android: Powers over 3 billion devices worldwide, dominating the mobile operating system market.

Google Cloud: A fast-growing cloud computing platform, competing with Amazon Web Services (AWS) and Microsoft Azure.

Advertising: Google Ads and YouTube Ads account for over 75% of Alphabet’s revenue, leveraging its vast user base.

Other Bets: Includes Waymo (autonomous vehicles), Verily (life sciences), and DeepMind (AI research), representing high-potential growth areas (https://x.company/) «< I will get to this a bit later.

Alphabet operates through three main segments:

Google Services (search, YouTube, Android)

Google Cloud

Other Bets, with a strong global presence across the United States, Europe, Asia-Pacific, and beyond (Seeking Alpha).

When you discuss Google and the way they monetize things, you will often get the refrain that they are a dying company because they rely too much on search. To offer a brief anecdote regarding this point, I used to make some decent money back in the day creating websites and using SEO to rank them. Everyone used to tell me that nobody actually clicks on those little blue links or intrusive adverts. But let me tell you, people would absolutely click on those ads all day long.

I am well aware that times are changing and online habits are evolving, but the point I’m making is that just because you or your social circle don’t do something doesn’t mean that others also don’t.

A case in point is YouTube Premium. Not long ago, many people claimed they would never pay for a service like YouTube, but today it certainly seems that YouTube is generating a significant amount of revenue from subscriptions.

Obviously, this is purely anecdotal but should give you a bit of an idea of how you would do well not to always follow the herd.

Google X (It’s Not Just Elon Who Loves Xs)

I won’t spend too much time discussing Google X, also known as their so-called “moonshot” division, since it hasn’t always made money in comparison to their other plays.

Nevertheless, it is a fascinating insight into how this company thinks, i.e., looking to the long term rather than the here and now.

X’s portfolio includes both projects that have graduated into independent companies and ongoing initiatives that push technological boundaries. Below is a summary of notable efforts:

The interesting part about the entire moonshot idea is that the projects tend to be based around targeting critical global issues, including

Connectivity

Transportation

Energy

Automation

Or, in other words, all of the sorts of things that are vital for civilization to continue to move forward at a decent clip. The most famous is undoubtedly Waymo, which is currently operational and drawing in extensive data from real-world testing that can and will be used to improve how self-driving vehicles work.

Even projects that don’t succeed commercially, like Project Blixt, generate valuable scientific insights, as X plans to publish its fusion research data.

Looking at things through a more strategic lens, X diversifies Alphabet’s portfolio, reducing reliance on advertising revenue and positioning the company to capture new markets.

The downside to all of those lovely upsides is that Alphabet allocates significant resources to it, including money as well as talent. Even with their substantial bank account, the fact that they are funneling so much toward projects that might never make money can be concerning to some.

However, I see it as a hedge against future developments, and in my opinion, this is money well spent and an approach that other tech companies should follow to make use of their enormous piles of cash.

AI

We can’t talk about Google and leave out the elephant in the room, which is that small thing that nobody has really mentioned, I don’t know, maybe a trillion times over the past few years: AI.

Many will state that Google was late to the game when it came to AI, being outmaneuvered by OpenAI with their ubiquitous ChatGPT.

This is a little unfair, though, IMHO. While they may have been late bringing what they had to the consumer in a way that OpenAI managed to do, how they have worked to remedy this recently has been nothing short of a masterstroke of management.

With the latest updates in Android (which Google also happens to own), they have begun to integrate it heavily into the mobile OS ecosystem.

Additionally, they have begun integrating it heavily into their other existing platforms, notably Google Drive. And, as someone who uses Drive extensively, I can tell you from personal experience that it is great!

If you’re still not convinced, just listen to the “podcast” audio I generated using the Gemini Deep Research feature. (I’m neither American, nor do I have any friends to podcast with.)

I mean, if your mind isn’t completely blown yet, I really don’t know what else to say!

VEO 3

VEO 3 is Google’s latest AI video generation offering, and by all accounts, it’s one of the best in existence. I’ve personally seen some of what it can produce, and although I didn’t see how they prompted it to create the scenes, they were created by a normal person, not some Google engineer (meaning that it’s unlikely there was any sort of trickery involved to create the outcome).

They have also locked it and many of their other advanced AI models behind a $250 “AI Ultra” plan, showing an increasing ability to monetize what has thus far been eating cash. This is in stark contrast to OpenAI, who may have gotten the first-mover advantage but are soon finding out that when the Google ocean liner starts moving, there is very little to stop its momentum.

“Bruh. We are so cooked.”

YouTube Commenter: maxcomperatore

Risks and Challenges

Now, in the interests of fairness, it’s not all roses and cheese sandwiches.

Google faces some pretty intense issues that could yet derail this love-in. But as you will read in a moment, some of these issues have interesting wrinkles that could save the day for them.

While Alphabet’s outlook is positive, investors should consider the following risks:

Regulatory Scrutiny: Alphabet faces antitrust lawsuits in the U.S. and Europe, including a 2024 ruling that Google illegally monopolized the search market. Potential fines or structural changes could impact operations (The New York Times).

Competition: Emerging AI-driven search alternatives (e.g., ChatGPT, Perplexity) and social media platforms like TikTok could challenge Alphabet’s advertising dominance (TheStreet).

Advertising Dependence: Over 75% of revenue comes from advertising, making Alphabet vulnerable to economic downturns or shifts in digital advertising trends.

High Investment Costs: Alphabet’s $75 billion planned investment in data centers for AI in 2025 could pressure short-term profitability (Financial Times).

Now let’s get to that wrinkle. There are plenty of people that say Google is cooked thanks to the plethora of AI search services that are coming to eat their lunch. To avoid this point would be silly, because they are undoubtedly taking a chunk out of Google search (which Google hasn’t helped by seemingly making search a terrible experience these days).

But the fact of the matter is that if AI is chipping away at them, that means they have competition and thus have a stronger argument to fight against a forced breakup.

However, it's important to note that the Justice Department will ultimately reach their own conclusions. But I just think that they have sound arguments to remain operating as they currently do.

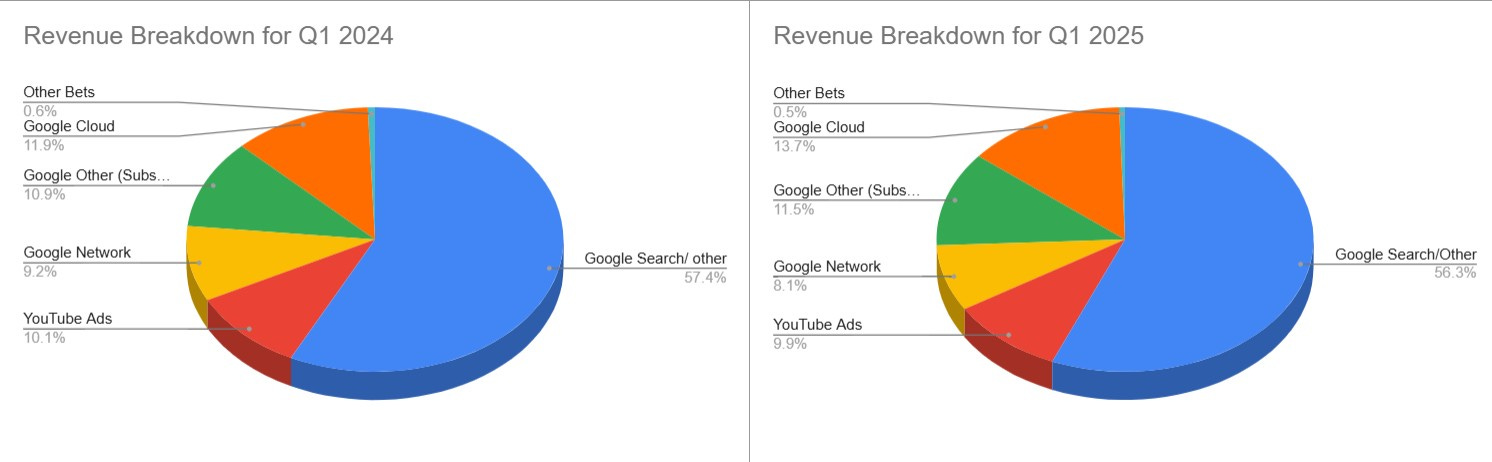

Now, the dependence on advertising revenue is worrying, but if you look at the charts below, they are reducing this dependency and slowly diversifying their revenue streams.

Financial Data

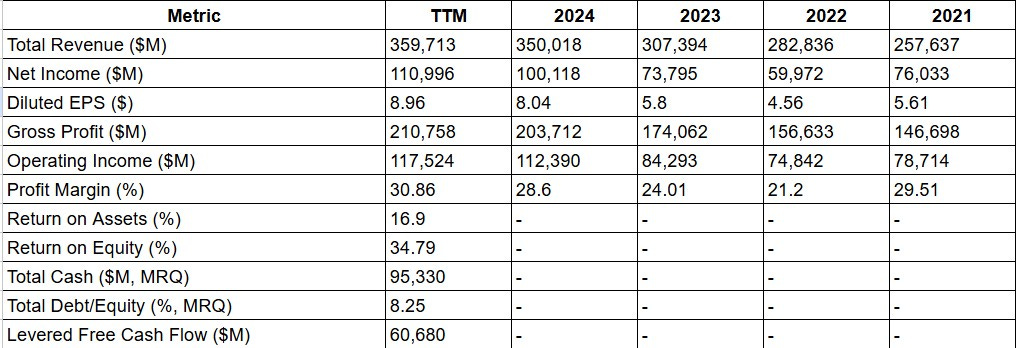

Alphabet’s financial performance underscores its strength as a leading technology company. Below are key financial metrics for 2024 and the trailing twelve months (TTM) as of May 2025:

Revenue Growth: Alphabet’s 2024 revenue of $350.02 billion reflects a 13.87% increase from 2023, driven by strong performance in advertising and cloud services (StockAnalysis.com).

Profitability: A 30.86% profit margin and 34.79% return on equity highlight Alphabet’s ability to generate substantial profits from its operations.

Financial Stability: With $95.33 billion in cash and a low debt-to-equity ratio of 8.25%, Alphabet has significant financial flexibility to invest in growth initiatives (Yahoo Finance).

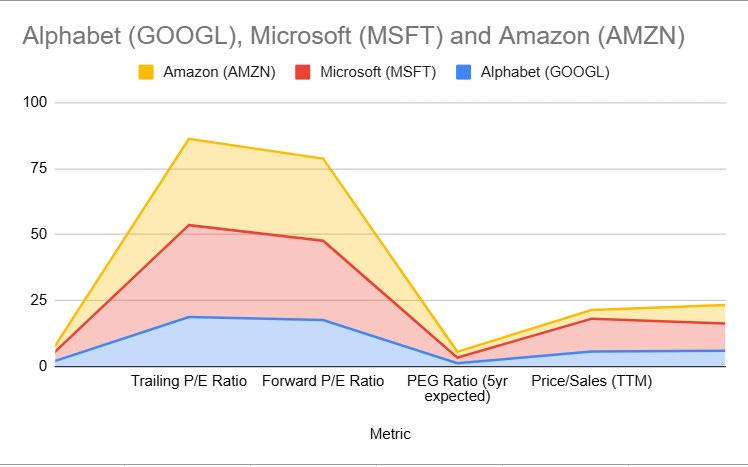

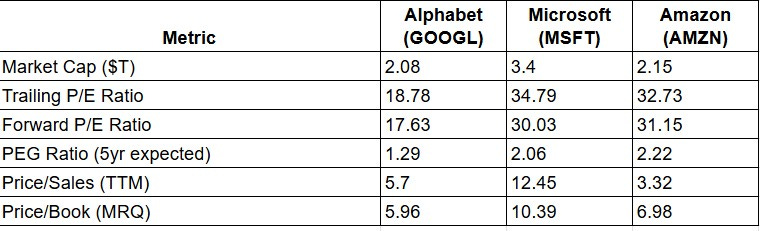

Alphabet’s valuation metrics suggest it may be undervalued relative to its peers:

Analyst Opinions

Analysts are optimistic about Alphabet’s stock:

Consensus Rating: "Buy" from 43 analysts, reflecting confidence in Alphabet’s growth and financial strength (StockAnalysis.com).

Price Target: The average 12-month price target is $200.66, implying a 19.11% upside from the current price. The range spans from $159 to $240 (StockAnalysis.com).

Key Insights: Analysts highlight Alphabet’s AI advancements, cloud growth, and undervaluation as reasons for optimism. Goldman Sachs’ Eric Sheridan maintained a "Buy" rating with a $220 target (StockAnalysis.com).

Why GOOG/GOOGL Could Be a Good Investment

Alphabet presents a compelling case for investors due to several factors:

Undervaluation: With a P/E ratio of 19.07, Alphabet is more attractively priced than peers like Microsoft (35.15) and Amazon (33.24), offering value for a company with strong growth prospects.

Robust Financials: Consistent revenue growth (13.87% in 2024), high profitability (30.86% margin), and strong cash flow ($60.68 billion TTM) provide a solid foundation.

Market Leadership: Alphabet’s dominance in search and advertising, combined with its growing presence in cloud and AI, ensures a competitive edge.

Growth Potential: Investments in AI (Gemini, DeepMind) and cloud services, along with ventures like Waymo, position Alphabet for future growth.

Analyst Confidence: A "buy" rating and 19.11% upside potential reflect strong analyst support.

Financial Flexibility: With $95.33 billion in cash and low debt, Alphabet can fund innovation and potentially initiate dividends in the future.

However, investors should weigh these positives against regulatory risks and advertising dependence. Alphabet’s diversified portfolio and strong fundamentals mitigate some of these concerns, making it a balanced investment option.

Fin

So where do we stand with all of this data and conjecture? Well, I genuinely believe that Alphabet (GOOG/GOOGL) is a strong investment candidate due to its market leadership, robust financial performance, and growth opportunities in AI and cloud computing. While regulatory challenges and competition pose risks, its attractive valuation and analyst optimism suggest significant upside potential. For long-term investors, Alphabet offers a compelling blend of stability and growth in the dynamic technology sector.

However, as always, this is purely my own opinion based on the research I perform based on the way I like to invest.

I strongly recommend conducting your own due diligence that aligns with your time horizons, your investment capacity, and your preferred investment approach. Keep in mind, building wealth is a gradual process. Building wealth is a marathon, not a sprint.