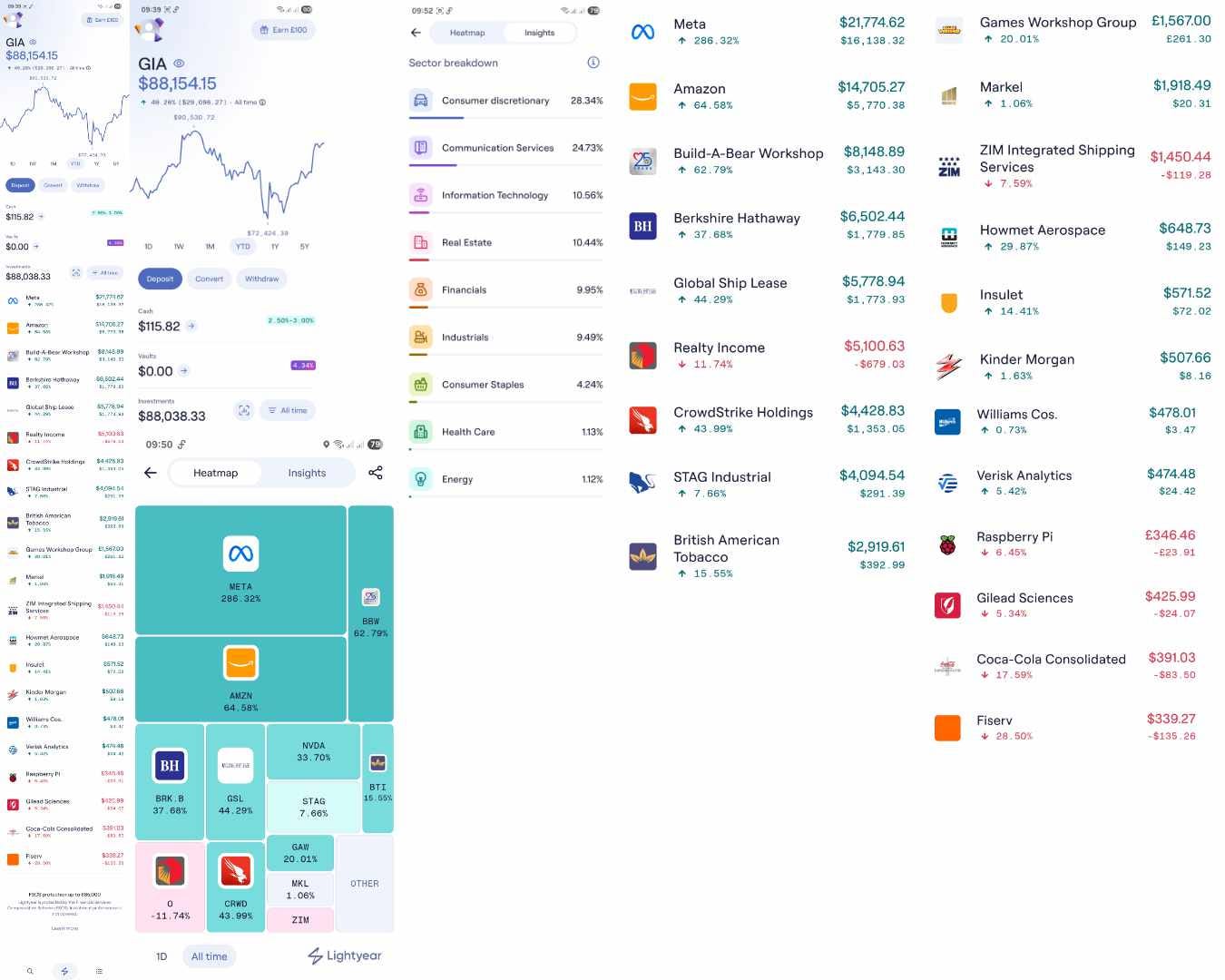

My Current Portfolio

A dive into my personal portfolio and the reasonings behind my selections

Having spent a considerable amount of time in the field of online stuff and finance in particular, I've come to understand that all claims are mere rhetoric until they are supported by tangible evidence. To that end, I am creating this post to hopefully allay your fears regarding whether I practice what I will eventually preach! This initial post (which I will pin for future reference) will show my current portfolio, along with a simple summary of why I chose to invest in each of my positions.

Right, so that is a lot to take in at one moment, but let me explain each position in turn. Before I begin, I would like to clarify that the app I use, Lightyear, is accessible for both British and various EU nations. Just note, though, that, although it’s a fabulous app to use in terms of ease of use and UX, it lacks a DRIP feature (meaning that you have to reinvest any dividends manually) and is missing a few tickers, which can be frustrating when you find a great option.

The first thing you might notice is that I am heavily invested in US equities. This arrangement is fine for my level of risk, but if you have less of an appetite for risk, then you may want to spread your positions across multiple countries. Nevertheless, let’s get into each position.

Contents:

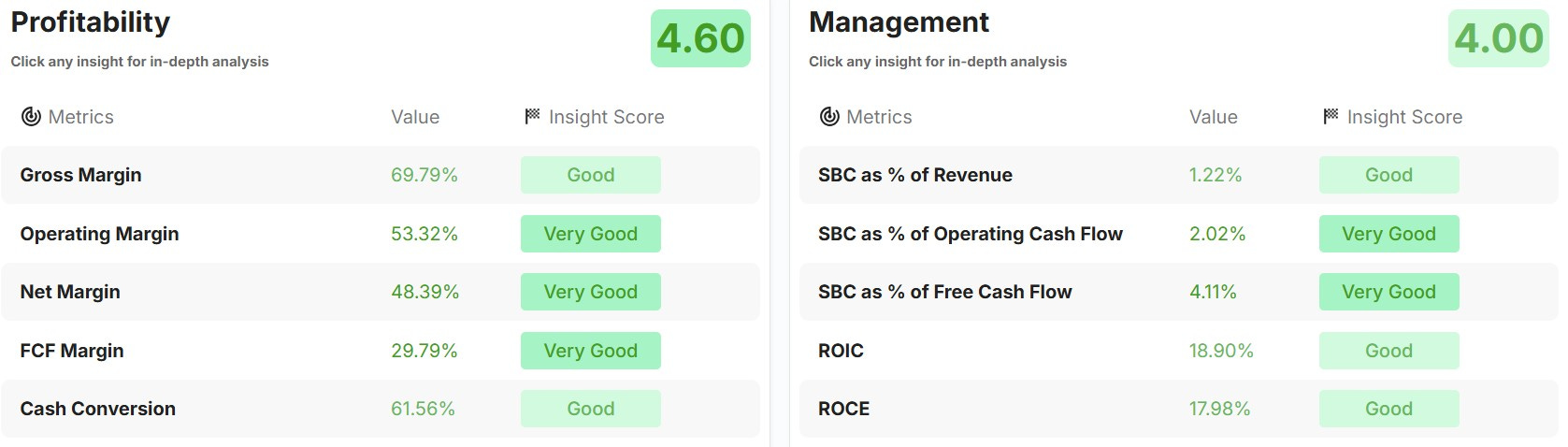

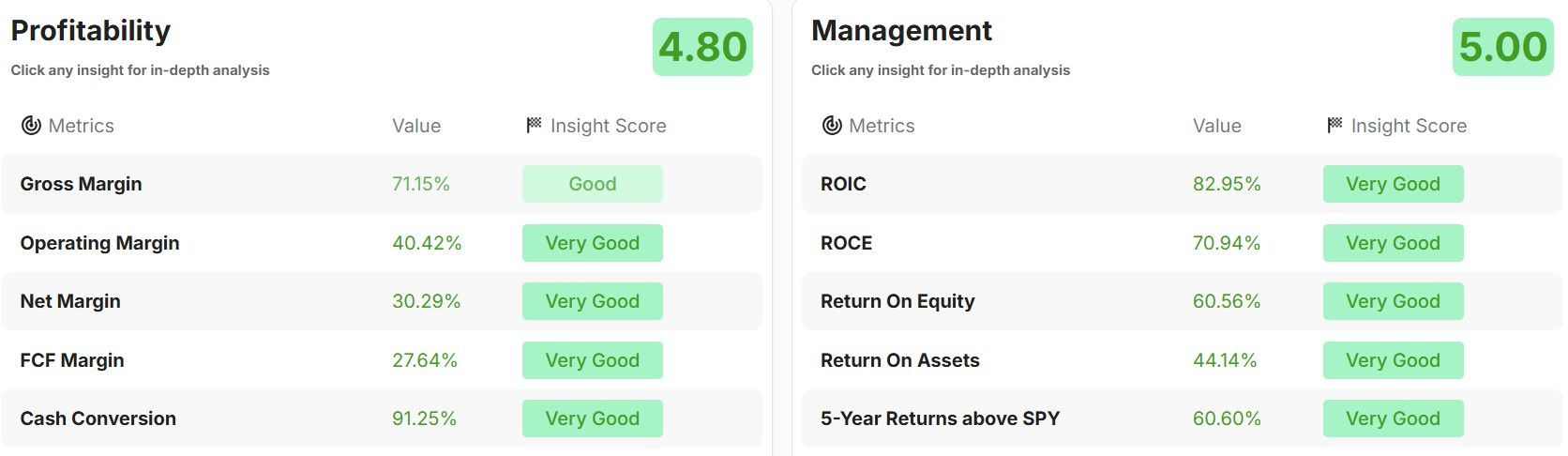

Meta (META)

This is my best-performing stock, and it makes me regret not investing more; however, that’s just how investing goes! The reason I chose to put so much into Meta is actually a pretty intriguing story. I entered heavily into this position in 2022 when the company noted its first-ever dip in users. The stock had been on a downward trend, decreasing from its most recent high of approximately $378 to a low of around $80. I love to see these drops, especially from a company that you know has so much potential.

I was mulling over when to enter, and for me, the time came when it hit $117. So suffice it to say, I loaded up the truck (for my financial ability) and bought 34 shares. The question is why, though?

It was a combination of factors that included the fact that after spending some time looking through the numbers, the dip in subscriber count and subsequent reaction seemed to me to be somewhat of an overreaction. However, the point that pushed me to make the jump came when I saw my daughter playing with her Roblox account. I will copy a Reddit comment I made in the r/stocks subreddit where I explain my reasoning:

I have a 9 year old daughter who plays Roblox which you could say is a kind of metaverse sort of thing. While I don't pay for anything on it, I know plenty of other parents who willingly allow their kids to buy the in game currency to buy a whole load of random stuff related to the game.

I remember when Facebook or Meta tanked hard a couple of years ago because investors were concerned about the sheer amount they were and still are spending in their version of a metaverse. But when I saw my kid and many others spending time and money on this stuff, it appears to me that Meta is building a foundation for their future revenue and along with their already solid fundamentals, I took a punt and bought a fair amount at an average of 114 and have just sat back and watched it surge over the years.

Have I managed to replicate this success with other businesses? Not yet, but it has changed my whole mentality of investing and I am more comfortable to spend more time investigating a company beyond just the numbers.

https://www.reddit.com/r/stocks/comments/1euapw1/what_insights_trends_did_you_see_when_making/

So while I very much like to think of myself as a long-term value investor that focuses on the fundamentals above all else, I strongly believe that there is more to a company than just the numbers.

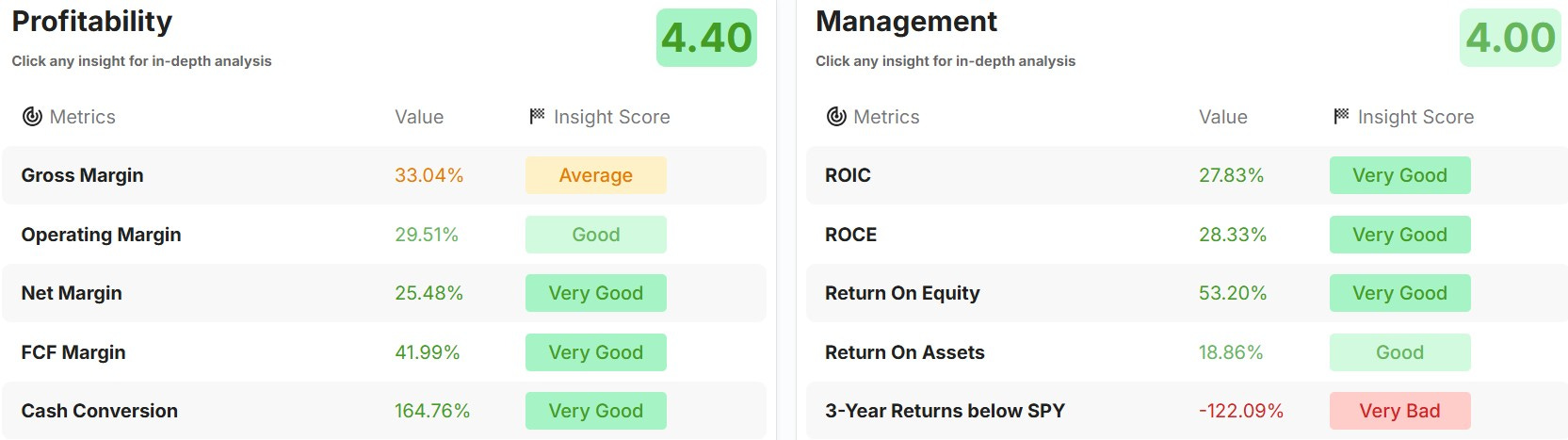

Amazon (AMZN)

My next largest position is with the company we all love to hate but all use all the time nonetheless: Amazon!

Amazon is the epitome of a fantastic business in my opinion. Regardless of whether one loves or hates Amazon's practices and their seemingly endless ability to manipulate their financial records to minimize their tax burden, the reality is that they generate substantial profits and maintain a global user base, including in India, where they successfully outcompeted a local alternative—a significant achievement given the challenges of doing business in that market. Although it is seeing fierce competition in that country, it still has a strong presence as well as almost total domination over most Western nations.

It’s also a powerhouse when it comes to streaming, and the way they attached their subscription model to their Prime offering is a masterstroke. They gain legions of loyal consumers who are willingly offering their cash and their data all for the allure of next-day delivery and Clarkson’s Farm!

The point is that, despite the ongoing tariffs and trade wars that look like they will rumble on for some time, Amazon's numbers continue to rise, and there appear to be no signs of a slowdown.

Build-A-Bear Workshop (BBW)

BBW might come across as a peculiar business to get involved with, particularly as there isn’t much written about them elsewhere. At first glance, it looks like they’re an old-school business that has no place in the modern world and will likely die a slow death over time. But if you look a bit more deeply into their business and how they’re doing, you’ll see a very different picture.

I got into this position after using a screener and they are one of my first investments that I have let run and not touched (only to buy more during the dips, which I’ll come back to later and reinvest the dividends). If you look at their numbers, they are very successful and capable of bringing in decent revenue over time.

The reason I really chose to invest outside of pure number crunching was due to their incredibly competent management. They have one of the best management teams I have seen in a company and have a refreshing take on doing business.

They’ve had plenty of dips and peaks, but the thing that endeared them to me was listening to their earnings reports. I remember that before their first dip (in terms of my investment in them), they made pains to note that they had a long-term plan that was going to be tail-heavy. I.e., they were investing now for a positive outcome later in that year. And, lo and behold, most of the more important things they said came true during the time period they mentioned.

Despite my strong belief that their current price is at its peak and I won't be investing in them beyond dividends, I am content and will regularly monitor their performance. I will also do a deep dive into them at one point or another, which might not convince you to buy them directly but should give you an idea of my thought process and what to look out for when searching for your own winners.

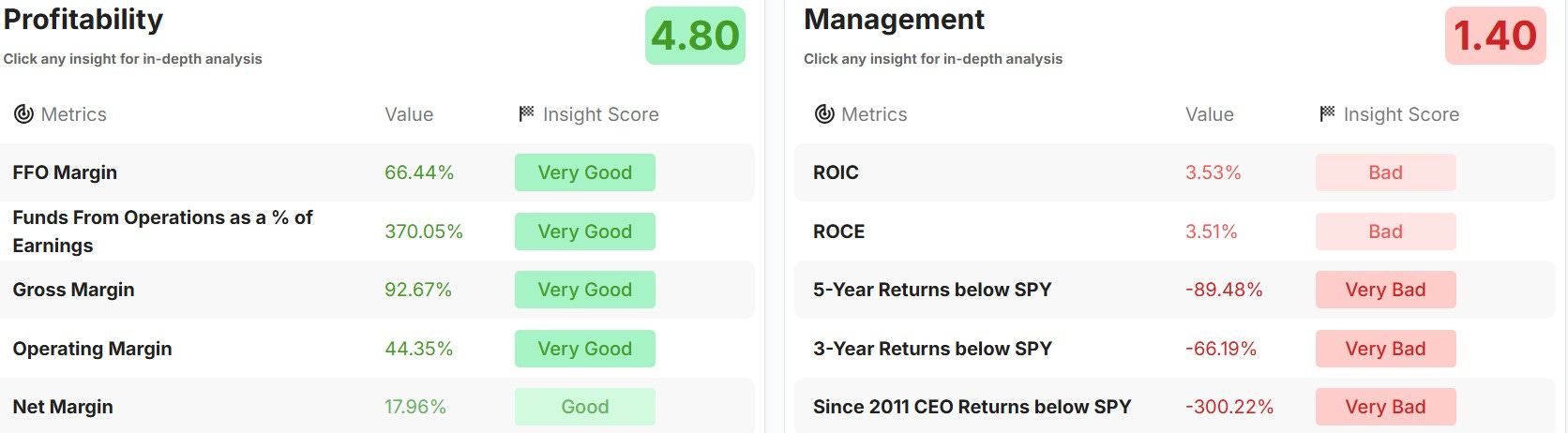

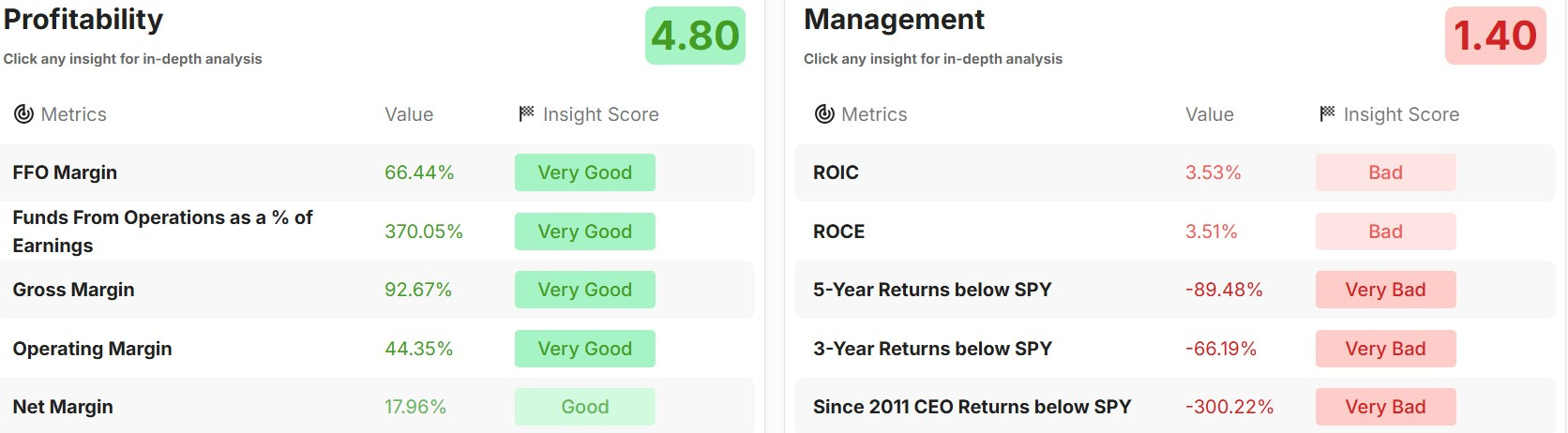

Berkshire Hathaway (BRK.B)

The one, the only!

If you’re not currently invested in some way in this company, you should do your research and make a choice as soon as possible. This firm is really the epitome of a buy-and-hold-forever type of stock and one that is almost universally praised for its approach to business and ability to make money for those who appreciate this sort of investing. It’s fair to say (if not a bit morbid) that once the oracle of Omaha himself passes away, there will be some turmoil, but for those who are in the know, that will simply mark a point to back up the truck again.

Warren Buffett has elected his successor in Greg Abel, who is Abel in name and able in nature, it seems. Therefore, the company appears to be in good hands for the long term. I don't have much more to add, except that it is worth considering, and for those with a long-term perspective, it has the potential to help you build wealth.

Just as a quick aside, and something interesting to note about BRK.B, is that I live in Laos and they have a Chinese-built high-speed railway that operates from the north of the country to the capital city. I have noticed that all of the major stations along the railway line have a Dairy Queen (which happens to be a wholly owned subsidiary of Berkshire Hathaway), which appears to be quite popular.

My point being, that if they are able to place an American company (albeit likely franchised by a local operator) in the Chinese-built station of one the last remaining Communist countries in the world… I think they know what they’re doing!

Global Ship Lease (GSL)

If I am being entirely honest, I got into this company for the dividends without expecting loads of growth, but luckily for me, it turned out well (which isn’t always the case, as you will see later with ZIM and O). To cut to the chase, it’s a great company that is essentially a holding company, which owns and charters out containerships under long-term and fixed-rate charters to container shipping companies. Although they possess strong fundamentals, they are also susceptible to sudden changes in market conditions. Nonetheless, a fantastic business run by a competent executive team.

Realty Income (O)

great company, simple ticker, and a business that is relatively consistent in what could be classed as a relatively volatile space. Long considered the holy grail for dividend investors thanks to their monthly dividend that has increased for the past 30 consecutive years, O is a stalwart for those seeking a dependable monthly income from their investments. This was one of the first companies I ever invested in and have been reinvesting the dividends ever since (and will continue to do so forever, probably).

Admittedly, I didn’t conduct extensive research at the beginning of my investing journey, but this is one of the few investments that I am glad I made. Would I recommend others to invest? The jury’s still out on that one, but I do like the company, and they have remained consistent over the years so keep it, I shall.

Crowdstrike Holdings Inc (CRWD)

Never invest in companies if you don’t understand what they do. That is sage advice from Mr. Buffett and is undoubtedly true…for the most part. While I tend to follow this advice, I chose to jump into this stock just after they caused a massive, worldwide IT outage that inflicted plenty of pain and distress on the world’s already overstretched IT admins.

You might be thinking that that was the worst possible time to invest, when a company hits all-time lows due to an easily identifiable mistake that should never have occurred. Well, dear readers, as long as you do your research, you can find some bargains where once there were none.

The story intriged me so I did a bit of sleuthing and it transpired that here is a business that lots of other businesses rely on for their cybersecurity demands. Not only that, but according to those who use the platform (which consists of several different products), it is also a very sticky product that isn’t easily replaced.

After looking at their subscore count and business before the crash, paired with my own fundamental analysis, I deemed that the plunge in share price was your bog-standard market reaction.

Was it a risk to jump aboard what looked like a sinking ship? Probably. However, the reality is that it was never truly a sinking ship, and despite the ongoing threat of never-ending legal action from those impacted, it continues to be a solid business with a very loyal user base. loyal user base.

NVIDIA (NVDA)

Just as a quick update, I forgot to add what is possibly my most soul-destroying stock and the one that taught me that value investing is the way forward.

To cut a long story short, I used to playu options and as you may or may not know, if you want to sell calls or puts, you need 100 shares of a given stock. I bought 100 when they were around 170-ish and used options to get the premium on the play. Then, the shares were called away, which was fine for me at the time because I still made my premium and a little more than what I originally paid for them.

The only issue is that almost a month after this happened, NVIDIA had their moonshot moment… and I was down 100 shares.

To put it succinctly, playing a game I was unfamiliar with resulted in a significant loss of potential income.

Anyway, fast forward to the last couple of years; I have bought and sold here and there. I bought more when they dipped due to the DeepSeek fiasco (which turned out to be a mere pause for thought rather than a massive turning point in the world of AI).

I also bought a whole lot more after Mr. Trump's Liberation Day tariff thing that he dropped on the world. NVIDIA dipped out of fear of losing sales, but as with all things of this nature, it turned out to be transitory.

The main lesson for me is that if a business's fundamentals are sound and they are making money sustainably, then there is no reason to fear the dips.

STAG Industrial (STAG)

Here we have a REIT that operates lots of locations around the USA. What initially attracted me to them was their model that focuses on industrial buildings like warehouses and factories, which are less affected by a downturn in property than residential or office-based buildings (the former because of house pricing fluctuations and the latter because of the continuing difficulty of getting people back in the office).

STAG also counts Amazon as one of its primary customers (its largest, in fact). The situation could potentially be detrimental if Amazon chooses to go its own way, but as of today, I like this business.

British American Tobacco (BTI/BATS)

Investing in the tobacco industry can be a bit of a contentious subject for most, but I live life very much on the basis that if a consenting adult knows the risks of something, they ought to be allowed to crack on.

Anyway, this was another of my initial investments, and I used to have a pretty substantial allocation, with BTI being my largest position for quite some time. I like the dividends, and I like how they are slowly transitioning themselves for a dramatically reduced user base. The only reason that I stopped investing in them and even cut my position to what it is today is because the brokerage app I used chose to stop allowing me to invest in the ADR BTI version and forced me to instead use the LSE: BAT version. I didn’t like this option, as it involved me liquidating the BTI position and reinvesting in the FTSE BAT position. Therefore, I cut my position to reallocate a lot of cash toward more growth-oriented stocks.

I keep the remaining position because it provides me with around $140 every quarter that I can invest elsewhere or let sit in the interest-accruing account.

Games Workshop Group (GAW.L)

Perhaps my favorite position based on pure emotion alone. I actually like Games Workshop and while I don’t play the tabletop game anymore, I still enjoy the lore. There are three things that convinced me to invest in GAW:

They have an incredibly diehard following.

There is a massive following in a number of developing countries that indicates a large, untapped market.

I knew that things would pop off and create a momentum when I heard that Henry Cavill is working with Amazon Studios to possibly create a feature film. Additionally, Amazon chose to include a brilliant episode of their Secret Level miniseries, which was widely and positively received.

Combining these points with the highly acclaimed Space Marine 2 game can lead to gradual success.

Markel (MKL)

This is a new one and based on my desire to diversify into different things and ending up with a choice between

Brookfield Corporation (BN)

KKR & Co. Inc. (KKR)

Markel Corporation (MKL)

I chose MKL due to its growth compared with the others and after reading the various earnings reports and listening to each manager. I landed on MKL because it just seemed to me to be the simplest of the lot and is invested in a range of insurance services that not many would want to get into due to their rarity but are highly lucrative (wink, equine insurance).

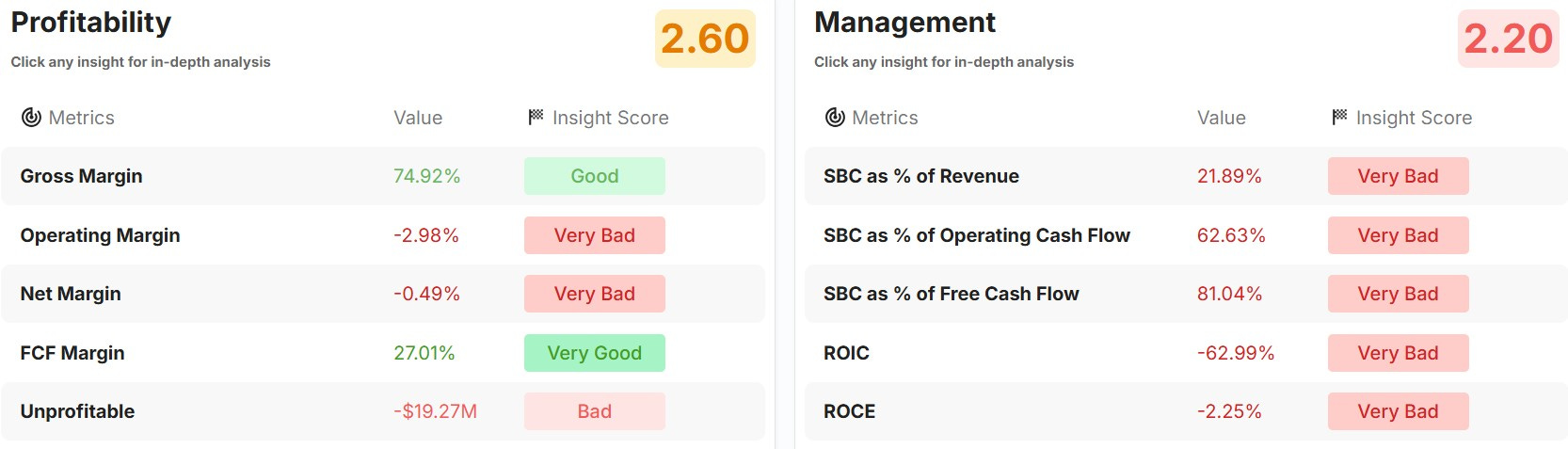

Zim Integrated Shipping Services Ltd (ZIM)

Oh, Zim, I love you, but I also hate you. I will be upfront and admit that I only invested because they had (have) a dividend yield that would make a gold digger blush.

I used to get hundreds of dollars each quarter from them until they made the (wise) decision to halt payments to focus on investing in the business. This decision was made in response to the negative supply chain environment following Covid, which ultimately led us into this period of high inflation. This led me to panic sell, which has proven to be my worst investing mistake so far. The company has reintroduced the dividend, which is a positive development; however, it still operates as a somewhat unstable business unless it is well managed. I will hold and continue to reinvest dividends.

Raspberry Pi Holdings PLC (RPI)

To keep an already long post as succinct as possible, I chose RPI because I think it has the potential to grow. I like the company, and my only real concern is that they are too British in their approach to business (I don’t think modern British enterprises have the same desire to succeed as US and Chinese ones).

However, for a small punt, it could blossom into something wonderful… We just have to wait and see.

Others

I have lumped the other 10 shares into one category because they are a test. I follow a company called MyWallSt (who offer a fantastic podcast you should check out), and they set up an investing platform called Prophet. They choose 10 companies and basically give you a sell, keep, or buy signal each month based on metrics they have found to work well.

I chose to invest $5000 ($500 in each of the 10 stocks) and see what happens. Obviously the entire market tanked after I did this so the current state isn’t exactly indicative of their previous results. But I like the way they invest so I will continue and see how it goes!

Fin

Phew, so that was a bit longer than I anticipated, but for my first post, it turned out to be a bit cathartic. It’s not often you can discuss your love for stocks and research with others, and when you do with those uninterested in building wealth, you tend to find their eyes glaze over!

Anyway, I hope you found this interesting, and I will slowly add more, including deeper dives into these stocks and others that I find interesting and potentially worth investing in.